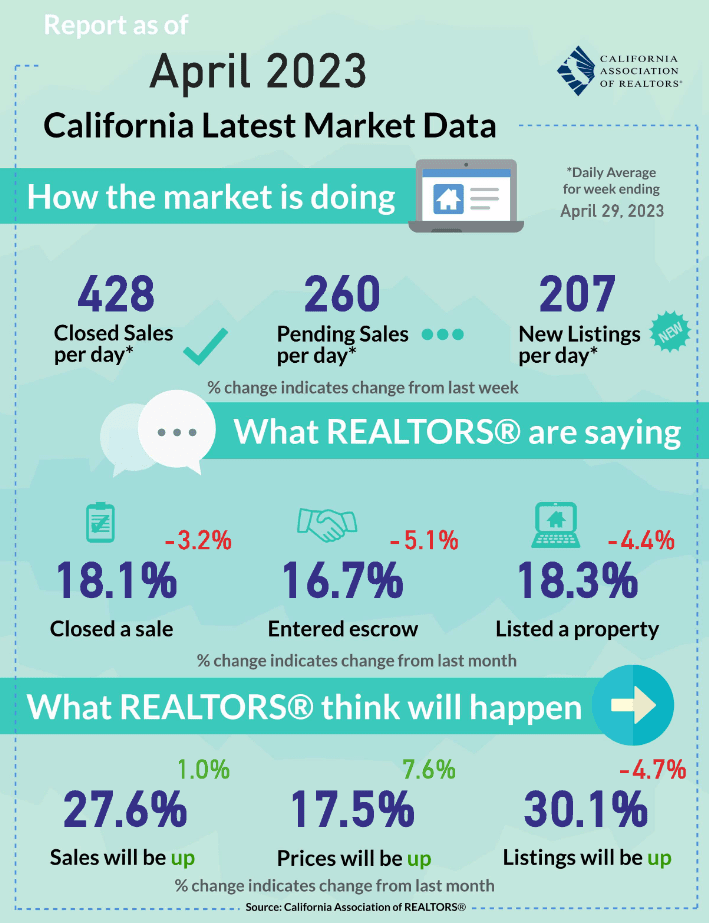

California April Latest Market Data

Housing Market CAR.org May 9, 2023

Housing Market CAR.org May 9, 2023

News from last week shows the economy continues to grow but doing so at a slower pace. The early reading for Gross domestic product (GDP) of the first quarter of this year suggests that the economy expanded but the momentum appeared to have fizzled out. When looking at retail sales and personal spending, consumers had been holding back despite real income improving nine months in a row. While a strong labor market continues to support wage growth, it also translates into higher labor costs and puts upward pressure on inflation. On top of that, recent bank failures added uncertainty to the overall health of the economy in the long run and suppressed consumer confidence in future expectations. As for the real estate market, the short supply of existing homes for sale steered more home-buying activity into the newly constructed housing sector, which comprised 33.2% of total single-family housing inventory in March – nearly double the 17.8% average in the year before the pandemic.

New home sales surge in March: Sales of new homes increased 9.6% from February to an annual pace of 683K as buyers turned to new construction amid low resale inventory. Although February’s sales gain was revised down to a 3.9% decline, March was the third increase in the last four months and the highest sales pace recorded in 11 months. The strong increase in sales made a dent in the months of supply of new homes, which dropped from 8.4 months in February to 7.6 months in March. It also resulted in greater competition and modest price gains. The median price for new homes rose 3.8% over the month and 3.2% over the same month of last year. Despite demand showing resilience in recent months, new home sales continued to run below their pace one year ago as interest rates remained elevated.

Consumer confidence falls as expectations about the future become uncertain: Consumer confidence dipped to a six-month low in April as growing concerns about the future and the stability of the banking system weigh on their sentiment. According to the Conference Board, the Consumer Confidence Index fell to 101.3 in April driven by a steep drop in the expectations component, which tumbled to 68.1 – the lowest reading since July. The drop in the forward-looking measure, triggered by fears of what lies ahead, could be a sign of pull-back on consumer spending in the near future. Meanwhile, the present situation index rose slightly to 151.1 during the same month, as consumers remained upbeat about both the labor market and business conditions.

The U.S. economy continues to expand, albeit at a relatively sluggish pace: Real GDP grew 1.1% at an annualized rate in Q1-2023 relative to the previous quarter. This was a step back from the 2.6% growth rate during the last quarter of 2022. The economic growth in the first quarter of 2023 was driven largely by a solid increase of 3.7% in real spending. Monthly data, however, shows that consumer spending might have lost momentum towards the end of the quarter, as retail sales activity dropped off significantly following January’s strong surge. Businesses also pulled back sharply in the first quarter, with inventories being drawn down, equipment purchases being cut, and residential investment being reduced.

Consumers’ reliance on credit and savings diminishes: The highest inflation in decades pushed consumers to rely on credit much more than in the past to sustain their spending. The six biggest increases in revolving credit in the last 20 years all occurred within the past 12 months. Credit is getting more expensive and more challenging to come by, however, as banks tighten up their credit standards due to recent bank failures. Moreover, although the personal savings rate rose to 5.1%, the highest in over a year, households are still saving a lower share of income compared to pre-pandemic levels. That said, income is still the real driver for most recent spending, and the tight labor market continues to provide support for wage growth. With inflation receding, real disposable income continued to climb for now and nudged higher for the ninth consecutive month in March.

Labor costs keep pressure on inflation: The Employment Cost Index (ECI) increased more than expected in the first quarter of 2023, with wages and salaries jumping 5.0% for the 12-month period ending in March 2023, while benefit costs rising 4.5% for the same time frame. With labor costs growing more solidly than anticipated and putting upward pressure on inflation, the Fed will likely raise the federal funds rate by another 25 basis points at the upcoming FOMC meeting on May 3.

Stay up to date on the latest real estate trends.

First Time Home Buyer

When a person passes away and leaves property to their heirs, the tax implications can be significant. However, U.S. tax law includes a provision known as the step-up … Read more

Marin County Housing Market

What's happening in the Marin County real estate market right now? March 2026 data on prices, inventory & trends in Kentfield, San Rafael & Novato.

Communities

Looking for the best San Rafael neighborhoods for families? Explore schools, safety, parks & home prices across Terra Linda, Sun Valley & more.

With integrity and a strong work ethic, we deliver a level of service at the forefront of today's real estate market. We offer the services of housing market experts, marketing specialists, and a home-closing real estate team, so your buying and selling experience is in clear view and at ease.