Tracking rents is important for understanding the dynamics of the housing market. For example, the sharp increase in rents helped me deduce that there was a surge in household formation in 2021 (See from September 2021: Household Formation Drives Housing Demand).

The surge in household formation has been confirmed (mostly due to work-from-home), and this also led to the supposition that household formation would slow sharply in 2023 (mostly confirmed) and that asking rents might decrease in 2023 on a year-over-year basis (now negative year-over-year).

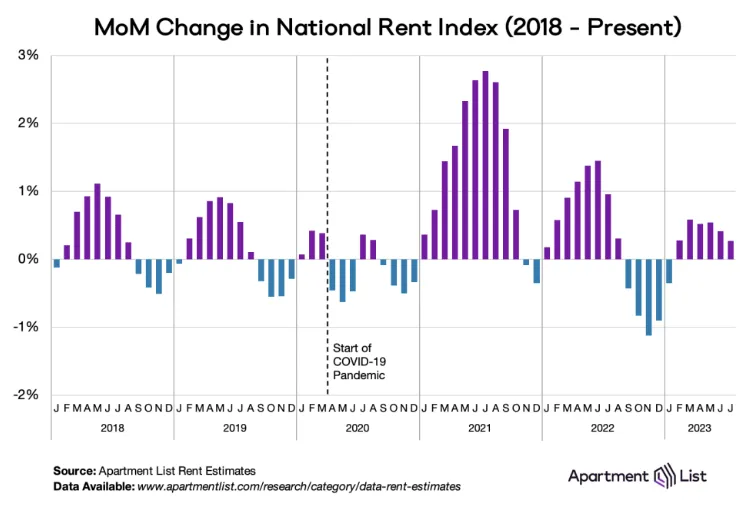

Welcome to the August 2023 Apartment List National Rent Report. The rental market hit a big milestone this month, as national rent growth is finally negative year-over-year. This means that on average across the nation, apartments today are renting for less than they did one year ago. This marks a major deceleration from recent years, when annual rent growth neared 18 percent nationally and soared to over 40 percent in a handful of popular cities.

On a month-over-month basis rents continue to tick up, albeit slowly. Our national rent index increased by 0.3 percent over the course of July, but this monthly measurement of rent growth has already peaked for the year. Rent growth in 2023 has come in at a much slower pace than previous years thanks to a combination of sluggish demand and increasing supply. …

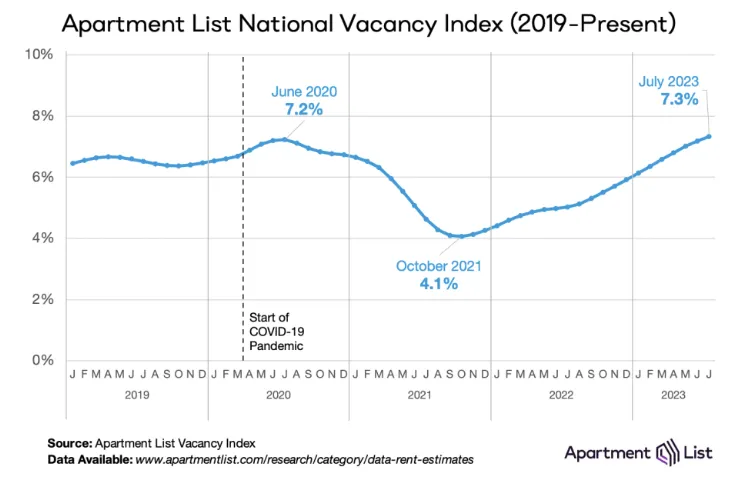

The supply side of the rental market also hit a major milestone this month: our vacancy index has reached 7.3 percent, surpassing the peak vacancy rate measured at the height of the COVID-19 pandemic. With a record number of multi-family apartment units currently under construction, this vacancy rate will remain elevated in the near future. For the first time since the early stages of the pandemic, property owners will compete for a smaller pool of tenants instead of the other way around.

Rents increased modestly in July in 71 of the nation’s 100 largest cities, but thanks to sluggish rent growth throughout the past 12 months, prices are down year-over-year in 67 of these 100 cities.

But after bottoming out in October 2021, our national vacancy index has been easing steadily for over a year and a half, and the rate of easing has picked up steam since last summer. In 2022, our vacancy index inched up an average of 14 basis points per month, but so far in 2023 the average increase has been 20 basis points per month. In July, the vacancy rate reached 7.3 percent, surpassing for the first time the pandemic peak set in July 2020.

This easing has shown no signs of slowing, and it’s likely that the vacancy rate will continue to trend even further upward in the months ahead.

emphasis added

Realtor.com: Second Consecutive Month with Year-over-year Decline in Rent

In June 2023, the U.S. rental market continued to see a year-over-year decline for the second month in a row, down 1.0% for 0-2 bedroom properties across the top 50 metros. The median asking rent was $1,745, down by $31 from July 2022’s peak but still up by $7 from last month and $339 (24.1%) higher than the same time in 2019 (pre-pandemic).

CoreLogic: “Rent Growth Returns to Pre-Pandemic Level in May”

Annual U.S. rent growth continued to ease in May, ending the month at 3.4%. Despite the past year’s continuously slowing rent growth, the overall rate of increase is roughly back to its pre-pandemic norm recorded between 2010 and 2019. …

“After increasing at an accelerated pace for more than two years, annual single-family rent growth returned to the pre-pandemic rate in May,” said Molly Boesel, principal economist for CoreLogic. “High inflation may be affecting renters’ abilities to absorb continually higher monthly payments, which could be keeping year-over-year rent increases relatively low. However, even in the current economic environment, monthly single-family rent increases returned to a typical seasonal pattern in February of this year, suggesting that single-family rents are poised to continue increasing throughout 2023.”

The 3.4% YoY increase in May was down from 3.7% in April.

Real Page: Rent Growth Remains Well Below Normal in 2023

Asking rents, meanwhile, continue to grow but at very muted levels – as they have in every month so far in 2023. Same-store effective asking rents rose just 0.46% between May and June 2023. That was the smallest increase for any June in the last decade aside from the lockdown period of June 2020.

Year-over-year, effective asking rent growth came in at 1.5%, the lowest since early 2021. Year-over-year rent change is now on pace to flatten or even turn slightly negative later this summer.

Rent Data

Here is a graph of several measures of rent since 2000: OER, rent of primary residence, Zillow Observed Rent Index (ZORI), ApartmentList.com and CoreLogic Single Family Rental Index (All set to 100 in January 2017)

OER and rent of primary residence have mostly moved together. The Zillow index started in 2015, the ApartmentList index started in 2017, and CoreLogic in 2004.

Note that new lease measures (Zillow, Apartment List) dipped early in the pandemic, whereas the BLS measures were steady. Then new leases took off, and the BLS measures have followed.

Here is a graph of the year-over-year (YoY) change for these measures since January 2015. Most of these measures are through June 2023, except CoreLogic is through June and Apartment List is through July 2023.

The CoreLogic measure is up 3.4% YoY in May, down from 3.7% in April, and down from a peak of 13.9% in April 2022.

The Zillow measure is up 4.1% YoY in June, down from 4.9% YoY in May, and down from a peak of 16.5% YoY in March 2022.

The ApartmentList measure is down at 0.7% YoY as of July, down from unchanged in June, and down from a peak of 18.1% YoY November 2021.

From Zillow:

“ZORI is a repeat-rent index that is weighted to the rental housing stock to ensure representativeness across the entire market, not just those homes currently listed for-rent.”

And from ApartmentList:

At Apartment List, we estimate the median contract rent across new leases signed in a given market and month. To capture how rents change in a market over time, we estimate the expected price change that a rental unit should experience if it were to be leased today.

Both of these measures reflect new leases, whereas most rental units don’t turnover every year (as captured by the BLS measures). The sharp increase in new lease rates in 2021 and early 2022 has been spilling over into the consumer price index (as discussed in earlier article).

The Rent of primary residence was up 8.3% YoY in June down from up 8.7% YoY in May. The Owners’ Equivalent Rent (OER) was up 7.8% YoY in June down from 8.0% YoY in May. The YoY change in OER and in PCE housing have peaked, but will stay elevated for some time, even though asking rent growth has turned negative YoY.

CPI Shelter was up 7.8% year-over-year in June, down from 8.0% in May, and down from the cycle peak of 8.2% in March 2023. Housing (PCE) was up 8.0% YoY in June, down from 8.3% in May, and down from the cycle peak of 8.4% in April 2023.

Conclusion

With slow household formation, more supply coming on the market and a rising vacancy rate, rents will be under pressure all year.